When searching for your dream home—and the mortgage to finance it—you must consider the cost of living in your area.

While cost of living does not necessarily align with home prices, it does affect your ability to qualify and repay your mortgage.

In this article, we will look at Canadian provinces with the highest and lowest cost of living. We will also look at the different factors that lenders look at when approving your mortgage. We'll outline guidelines to help you determine how much of a mortgage you can afford.

Provinces with the highest cost of living in Canada

Before we look at how cost of living can impact your mortgage, let’s first break down cost of living in Canada by province.

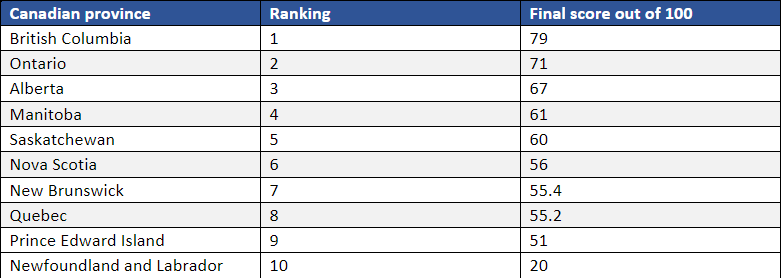

The province with the highest cost of living in Canada is British Columbia, according to a recent study by Westland Insurance.

The study looked at 55 contributing factors based on data from the Canadian Real Estate Association (CREA) and Statistics Canada. The contributing factors, which were divided into seven categories and given a score out of 10, included income, property prices, food, bills, rent, health and personal care, and transport. The scores were weighted and indexed to give a final score out of 100.

This graph breaks down the rankings and the cost of living scores by province.

Source: Westland Insurance

Next, let’s look at the different factors that impact the cost of living in each Canadian province. We’ll start with provinces that have the highest cost of living and work our way down.

British Columbia

Topping the list, B.C. ranked as the most expensive province for buying and renting property. While there are inexpensive areas to live in B.C., the province also had the costliest plane tickets, dental services, public transportation, hotel accommodations, clothing, and healthcare, among others.

B.C.’s housing prices are also the most expensive in the country, with a median price of $996,460 in 2022. That figure is more than double the national average home price, which was $490,520.

Ontario

The median home price in Ontario was $931,870 in 2022, with first-time buyers taking the longest in the country to save for a home. There are cities in Ontario where mortgage is cheap; but like B.C., Ontario also has the most expensive produce, furniture, and home repairs.

For the cost of renting and purchasing property, buying household appliances, and vehicles, Ontario ranked in the top three most expensive Canada-wide.

Alberta

Alberta is among the most expensive in terms of childcare, electricity, water, parking, fuel, groceries, and restaurants. For house prices, Alberta is the fourth most expensive in Canada (behind B.C., Ontario, and Quebec), with median home prices at $447,445. That is nearly a 10th below the national average.

Manitoba

The median home cost in Manitoba is below the national average at $360,373—making it 7th in this category. And among major expenses, Manitoba is also low. Costs of water, fuel, electricity, restaurants, childcare, pets, and vehicles in Manitoba are in the bottom three. However, Manitoba ranks fourth in cost of living with food and parking, among others.

Saskatchewan

The cost of housing in Saskatchewan is among the cheapest in Canada, with a median price of $303,261. This Prairie province ranks in the top three most expensive in the following categories: groceries, gas, childcare, vehicle maintenance, and pets. On the other hand, Saskatchewan is among the cheapest for buying and leasing vehicles, furniture, internet access, and household utility bills.

Nova Scotia

While this Maritime province is ranked sixth in highest cost of living in Canada, Nova Scotia has the fifth-highest median house price, at $411,784. Compared to other provinces, the cost of food is inexpensive in Nova Scotia, with groceries being the cheapest in Canada. Healthcare, including dental care, and personal care are also relatively cheap here.

New Brunswick

The median house price in New Brunswick is the cheapest in the country at $289,786. Other factors, including airfare, rent, public transportation, alcohol, hair care, and school supplies, are also the cheapest or second cheapest nationally.

At the other end of the spectrum, electricity and gas costs in New Brunswick are some of the most expensive throughout Canada.

Quebec

The median house price in Quebec is $483,573, making it the third highest in Canada. Healthcare and personal care costs are especially high in Quebec. And costs for rent, utility bills, household appliances, and alcohol are in the top three most expensive in the country.

To offset these costs, Quebec also has some of the cheapest everyday costs, such air travel, public transportation, gas, and internet access.

Prince Edward Island

The median home price in P.E.I. is $388,844, well below the national average. In other costs, this Maritime province ranks the cheapest or second cheapest in Canada, in food especially. Most personal care and healthcare expenses, including dental care, are also the lowest in the country.

Expenses such as gas, internet access, autos, and pets, are the most expensive nationally.

Newfoundland and Labrador

Newfoundland and Labrador has the lowest cost of living in Canada. First-time homebuyers enjoy some of the lowest property prices nationwide, with a median cost of $291,807.

Everyday expenses like rent, car buying, restaurants, childcare, pets, eye care, and dental services are also among the cheapest in Canada.

Mean products and utility bills, on the other hand, consistently rank among the most expensive nationally.

What affects the amount of mortgage a person can afford?

The cost of living in any given province or city in Canada directly affects the amount of mortgage you can afford. For starters, the more income you have to spend in other areas of your life, the less you will have for your down payment and monthly mortgage repayments.

Let’s explore the various ways your cost of living can affect your mortgage.

The impact of cost of living on mortgage qualification

Mortgage lenders each have their own criteria for affordability. However, your ability to buy a property depends mostly on a few different factors. Here is a quick look at four of these factors:

- Front-end ratio

- Back-end ratio

- Gross income

- Credit score

In this section, we will explore each of these different factors.

Front-end ratio

One determining factor that affects the amount of mortgage a person can afford is the front-end ratio, which is also called the mortgage-to-income ratio. Your gross income plays a major part in determining your front-end ratio. This is the percentage of your yearly gross income that you can use to pay toward your mortgage each month.

Four components usually make up your monthly mortgage payments. This is also called the PITI, which stands for principal, interest, taxes, and insurance. In this case, insurance includes both your property insurance and private mortgage insurance (PMI), depending on your mortgage.

A good guide is that your front-end ratio, based on PITI, should be 28% or less of your gross income. There are lenders out there, however, that allow borrowers to exceed 30%. In some cases, your front-end ratio can be as high as 40%.

Back-end ratio

Your back-end ratio is also known as the debt-to-income, or DTI, ratio. Your DTI calculates the percentage of your gross income needed to pay off your debts. These debts often include any credit card payments or outstanding loans, such as your vehicle or student loan payments. Since vehicle prices, for instance, differ between provinces, this is directly linked by the cost of living.

Let’s look at an example. If you pay $2,000 per month paying off debts and you earn $4,000 per month, your DTI is 50%. That means it is half of your monthly income.

A DTI of 50% is going to make it difficult to land your dream home. Ideally, your DTI should be less than 43% of your gross income. The formula for calculating your maximum monthly debt based on your DTI ratio looks like this:

[Your gross income] x 0.43 / 12

Gross income

Your gross income is the amount you earn before taxes and other financial obligations. It is your base salary plus any bonus income. It can also include self-employment earnings, part-time earnings, disability, benefits, child support, and alimony.

Credit score

Your mortgage lender, whichever type of lender you go with, has a formula for determining your level of risk as a prospective homebuyer. And a major ingredient in this formula is your credit score. If you have a low credit score, you will have to pay a higher interest rate or annual percentage rate (APR) on your mortgage.

If you want to purchase property soon, you will want to make yourself aware of your credit reports. Any inaccurate entries, for instance, take time to remove. You especially don’t want to disqualify yourself for a mortgage over a blemish on your credit score that is not your fault.

How much mortgage can I afford in Canada?

As we have seen, the mortgage you can afford in Canada depends on a few factors. While taking these into account, there are affordability guidelines that will help you determine the amount of money you should be putting toward your mortgage.

One of these guidelines, which is set out by the Canada Mortgage and Housing Corporation (CMHC), revolves around your mortgage principal, interest, taxes, and heating expenses. The acronym is PITH. Your monthly PITH should not exceed 32%. If you have a condo, your PITH also includes half of your monthly condo fees. This ratio is called your Gross Debt Service (GDS) ratio.

The second affordability guideline set out by the CMHC is that your total monthly debt, including housing costs, should not exceed 40% of your gross monthly income. Beyond housing costs, your monthly debt load includes car payments, card interest, and other loan expenses. This ratio is called your Total Debt Service (TDS) ratio.

High cost of living in Canada may not prevent homeownership

When shopping for homes, it is important to consider which provinces have the highest cost of living in Canada. Depending on your budget, and your ability to work remotely, for instance, you may be able to afford a much larger house by moving one province over. Being aware of the cost of living in your region can also help you budget and/or offset the costs of your mortgage.

If you want help navigating the areas with the highest cost of living in Canada, take the time to look at the mortgage professionals we highlight in our Best of Mortgage section. Here you will find the top performing mortgage professionals, including mortgage brokers, across Canada.

Does this information on Canadian provinces with the highest cost of living affect where you will buy a home? Are there any other factors you would consider? Let us know in the comment section below.